A pension fund aims to ensure members get a net replacement ratio that allows them to retire comfortably. While pension payouts are not meant to make the member “very rich” (that’s on the member), the payout ensures the member can afford a basic standard of living in retirement.

Pension payouts can be via lump sums or annuities, and depending on the pensioner’s needs, one or both can help. These monies come from either a defined benefit or a defined contribution type of pension fund structure.

A defined benefit promises a specific amount to be paid to the member, using a formula set by the employer. In this case, the risk of investing falls on the employer; they must ensure the plan is fully furnished and that any investments consider the risk and return objective of the employee or member.

For defined contributions, the employee or member contributes a fixed amount and their employer matches a portion of that benefit. With this pension plan, the member assumes the risk and must ensure the investments made match their risk objectives.

Whatever the plan or payout type, two things remain true for a pension fund:

- It owes the members that money in the pension funds (liabilities)

- It must try to beat inflation

Inflation can affect pension funds in the following 3 ways:

Reduce asset prices

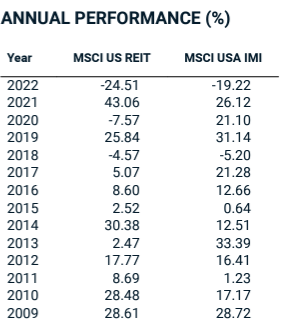

In 2022, when Russia attacked Ukraine, commodity prices skyrocketed, making stock markets drop as cash became king. Equities and bonds are two asset classes that pension funds mainly invest in.

The effects of inflation caused the below in 2022:

Equities dropped:

Source: MSCI

So did Bonds:

Source: Vanguard

Because pension funds prefer to have a high exposure to equities and bonds, when inflation is rampant, central banks take steps to curb inflation, such as by increasing interest rates. This can depress asset prices, ultimately reducing the asset value of the pension fund.

Reduce purchasing power

Inflation erodes the value of money. 20 years ago, $100 bought you more goods than it could today. Whether it is a defined benefit or a defined contribution, the pension fund aims to earn inflation-beating returns (i.e. positive real returns).

With high inflation and a poor asset allocation strategy, pending retirees would see the purchasing power of their money drop.

Let’s say Jay retired last month and has chosen to receive annuities of $2,000 monthly. In an economy where inflation is low and stable, that $2,000 allows him to live well, but not in a high-inflation economy.

Increase Liabilities

Pension funds owe their members. These liabilities are usually subject to inflation increases, with a cap. Therefore, if inflation rises, so do the liabilities.

Increasing these liabilities ensures that members’ pensions keep up with inflation. However, if inflation is too high, the cap is hit, and liabilities won’t be increased any further.

Asset-liability matching is pertinent because if your liabilities are growing but your assets are falling, the pension fund runs the risk of being underfunded.

Inflation hedging strategies for pension funds

Pension funds can leverage rising inflation with the right strategy in place. To illustrate this imagine two farmers: one with a good drainage system and dam in place, and the other with neither.

When it rains heavily, the farmer with a good drainage system and dam can avoid flooding and store water for future use. Some crops might be destroyed but chances of a total wipeout are reduced.

The farmer without the drainage system will see his farm flood and most of his crops destroyed. Inflation is the flood in this case and inflation-hedging asset classes are the equipment that can help reduce inflation’s effects.

Here are 5 asset classes that pension funds can enter to benefit from inflation.

- Real estate

Real estate is a fixed, physical asset — the land and buildings on it. During a high inflationary environment, you can increase rent on the property (even though it sucks for the tenant).

Rentals can hedge a pension fund against increasing inflation, depending on the type of real estate you have in your portfolio (e.g., retail, office space, hospitality, and residential real estate).

If it costs you $500,000 to build a house during a period of stable inflation, that amount will go up during times of high inflation due to increased building costs.

These costs translate to higher valuations, so while your rentals increase, theoretically, so does the value of your property. But in the real world, the value of property can drop sharply when inflation is high. I mean, look at 2022:

Source: MSCI

Why does this happen? Simple: when inflation goes up, central banks increase interest rates. Increasing interest rates mean loans become pricey.

Most houses are built or bought using mortgages. As mortgages become expensive, people may struggle to pay their debt, leading to property foreclosures.

Occupation rates also decline if tenants decide to go for cheaper alternatives. If you had taken a mortgage on the real estate and, due to low tenancy on your property, you cannot afford the mortgage, you might default on that loan, leading to a foreclosure and sale of the real estate. Therefore, as people sell their homes at reduced prices, the value of the property market goes down.

Inflation can affect real estate both negatively or positively depending on different factors. If done right, exposure to real estate can reduce the negative impact of inflation on a pension fund’s assets through rentals.

- Commodities

Commodities are good inflation hedges because we use oil to power our machines, metal to build things, copper for electricity, and animals and crops for agriculture and food. When inflation shoots up, these raw materials get more expensive, too.

Having exposure to commodities in your pension fund helps greatly with reducing the impact of inflation and giving your portfolio a positive return.

Source: S&P Global

- Equities

Some sectors do well during inflationary times. For example, when inflation goes up rapidly, so do interest rates. High interest rates deter people from borrowing money and entice them to save more. Since banks lend money and help people save, holding on to financial stocks might help in times of inflation.

But if the economy is really bad, people might default on their loans and banks may be reluctant to give out loans, reducing the bank’s growth and negatively affecting its share price. It is up to the asset manager to determine which bank stock is valuable enough to own.

Utility stocks are also good to hold during inflationary times as they are seen as defensive. Everyone needs electricity and water, so in good or bad times, utility stocks can help protect the portfolio’s performance.

Holding stocks of companies that deal in real estate and commodities also helps.

- Inflation Linked Bonds

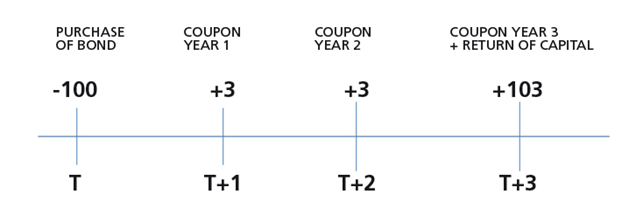

The typical bond structure is vanilla, where the pension fund purchases a bond and receives coupons for the life of the bond. When the bond matures, the pension fund receives its principal or capital plus the last coupon.

The coupons are fixed in such a situation. The coupon rate determines the coupon amount to be paid, and this rate is multiplied by the principal to get the dollar amount.

Therefore, if the principal is $1,000, and the annual coupon rate is 3%, then the coupon amount is $30. When inflation rises, this $30 does not change. The pension fund is worse off because even though things get expensive, it receives the same amount.

Let’s give an example of how inflation-linked bonds work:

Imagine a capital-indexed bond with a $1,000 capital, a 5% annual coupon rate, and inflation growing at 3% a year. The bond matures in 3 years.

Because it is linked to an inflation index, its capital rises in line with inflation while its coupon rate remains the same. Therefore, in the first year, the capital goes from $1,000 to $1030 (calculated as $1,000 x 1.03). The coupon paid in the first year would be 5% of $1,030 = $51.50.

In the second year, the capital goes from $1,030 to $1,030 x 1.03 = $1,060.9. The coupon on this would be 5% of $1,060.90 = $53.05.

In the final year, the principal goes to $1,092.73 and 5% of that would give us the coupon of $54.64. The investor would get that final coupon amount together with their $1,092.73.

If this bond was not linked to an inflation index, the investor would get $50 every year and $1,000 at maturity. With inflation protection, however, the investor gets a higher coupon amount and a higher principal at maturity.

- Hedge Funds

Traditional asset managers buy assets, wait for the value to increase, and sell when they deem it’s overvalued. If they hold on to stocks and markets fall, they lose money because the value of their investments falls.

Hedge funds can make money from markets dropping and rising. They can make money from any direction by taking long and short positions. Being long means you are buying and holding. Being short means you are selling securities now to buy them later at a lower price.

An example of going short is this:

Raj has done his research and predicts that inflation is going to increase and central banks are going to react by increasing interest rates.

Tech Company A (TCA), which uses a lot of leverage and depends on people to have a healthy disposable income, will be affected negatively because people won’t want to spend on its luxury goods.

Because of sales dropping, its stock price, currently at $67, will also drop. Raj thinks it might drop to about $30 in 6 months.

Raj borrows the stock of TCA from someone who owns it, and sells it now for $67. Six months later, Raj’s prediction is right and the stock price drops to $30.

He buys back the stock of TCA at $30 and gives it back to the investor he borrowed it from. His profit is $67 – $30 = $37, multiplied by the amount of stocks he traded. If he traded 10,000 stocks, that’s a $370,000 profit (excluding any fees).

The risk Raj faces is that the price goes up instead of down after he’s sold it. If it goes up, he would have to buy the stock back at a higher price — a loss for him.

The same premise holds for pension funds. Having a little exposure to hedge funds can help them during times of high inflation because as markets are dropping, hedge funds can make money:

Effective portfolio management in inflationary times

Pension funds should have a strategic asset allocation (SAA), and when the allocations deviate too widely, some rebalancing should occur. If the SAA was made for periods of stable inflation, and inflation increased drastically, then it might not be effective in the short term.

Tactical Asset Allocation (TAA) comes in handy here. TAA is a form of active investing where the investor changes allocations to take advantage of market conditions. The pension fund would then deviate from its SAA to take advantage of the current high inflationary environment.

So for example, if interest rates are increasing due to rising inflation, and the SAA states that the allocation to equities should be 40% and commodities should be 6%, it can reduce its equity exposure to 36% and increase its commodity exposure to 10%. This is because increasing exposure to commodities and less to equities may help its performance.

The allocation changes should be in line with regulations prevailing in the jurisdiction the pension fund is in.

For example, in Botswana, some rules stipulate how much can be invested offshore and locally and the exposure to each asset class. Therefore, when pension funds decide to implement a TAA, it must be in line with the prevailing regulations.

Active vs passive management during inflation for pension funds

When a pension fund navigates high inflation, the choice between active and passive investing becomes crucial, given their long-term horizon and fiduciary responsibility.

Active investing for pension funds:

Advantages: Active management allows pension funds to actively adjust their portfolios to capitalize on sectors that historically performed well during inflationary periods. They can target assets such as real estate, inflation-protected securities, commodities, and equities of companies with pricing power or resilient business models.

Passive investing for pension funds:

Advantages: Passive strategies offer cost-effectiveness and simplicity for pension funds, aligning well with their long-term objectives. Investing in broad-based inflation-protected bond indexes or diversified ETFs that hold inflation-hedging assets provides stability and a certain level of protection.

For pension funds, a blend of active and passive strategies might be ideal. Passive investments ensure stability and risk mitigation, aligning with the fund’s long-term obligations. Active strategies can be employed selectively to seize short-term opportunities and enhance returns.

The pension fund will need to consider risk tolerance, cost efficiency, and its obligations to ensure enough money to meet future liabilities.

Forecasting inflation: tools and techniques for pension funds

Predicting inflation with absolute certainty is hard due to complex economic factors and events.

Here are 5 ways a pension fund can prepare for it:

- Inflation models and forecasting tools: Financial experts within pension funds use sophisticated econometric models and forecasting tools. These models incorporate historical data, macroeconomic variables, and statistical techniques to predict future inflation rates. These models might involve Phillips curve analysis, time series models (like ARIMA), or more complex econometric models.

- Economic indicators analysis: Pension funds monitor economic indicators that can signal inflationary trends. Key indicators include the Consumer Price Index (CPI), Producer Price Index (PPI), employment data, wage growth, housing market trends, and monetary policy statements from central banks. Analyzing these indicators helps in assessing the current economic climate and predicting potential inflationary pressures.

- Interest rate expectations: Pension funds pay close attention to central bank policies and interest rate expectations. They analyze statements and signals from central banks regarding monetary policy shifts, as interest rates can significantly influence inflationary pressures.

- Scenario analysis: Pension funds can assess the impact of different inflation rates on their portfolio holdings, liabilities, and overall financial health. Stress testing their portfolios against different inflationary scenarios helps craft strategies to mitigate risks.

Lastly, if pension funds cannot do it internally, then,

- Outsource forecasting: Pension funds can rely on the expertise of economists, financial analysts, and researchers who specialize in macroeconomic trends and inflation analysis. These professionals analyze global economic developments and provide insights to guide investment decisions.

Case studies: Pension funds successfully managing inflation

Here are 3 pension funds that manage inflation effectively:

- CalPERS (California Public Employees’ Retirement System): CalPERS has navigated inflationary periods by diversifying its investments globally. They’ve allocated assets into inflation-hedging strategies like real assets (real estate, infrastructure) to protect their portfolio’s value during times of rising prices.

- Norwegian Government Pension Fund Global (GPFG): Norway’s sovereign wealth fund, GPFG, has a significant portion of its portfolio invested in real assets globally. They’ve allocated funds to real estate and infrastructure projects that tend to perform well during inflationary periods.

- The Abu Dhabi Investment Authority (ADIA): The ADIA is one of the world’s largest sovereign wealth funds, and has a long history of successfully navigating volatile markets. It is invested in various assets, including equities, real estate, hedge funds, private equity, and infrastructure. This diversification helps protect the ADIA’s portfolio from inflationary pressures.

Stay ahead of inflation as a pension fund manager

To beat inflation in pension funds, the fundamental premise is to maintain strategic asset allocation over the long term through exposure to asset classes or instruments that do well during inflationary times.

This manages inflation risk by increasing the asset value of the pension fund while other asset classes fall — one of the premises of diversification.

Setting inflation targets (e.g., CPI +3%) allows the pension fund to track its performance relative to inflation. Beating inflation is good, but a pension fund should strive to earn returns well above inflation.

An asset consultant helps pension funds or institutional investors strategize how to manage their investments and ensure healthy returns. Reach out to one to ensure your pension fund is protected from the harsh effects of inflation.