“If I loan you this money, return it with 20% interest.” — Your colleague.

“Back in my day, $100 bought a lot. Now, that same $100 buys so much less. That’s inflation for you.” – Your grandfather.

Depending on where you stand, inflation and interest rates can either grow your wealth or erode the value of your wealth. This article will take you through the basics of inflation and interest rates, their definitions, how they work in the context of investment and debt, and their relationships with each other.

Interest Rates

An interest rate is a percentage that a lender charges a borrower. This interest rate is charged on the principal (the amount borrowed) and used to compensate the lender for foregoing their spending now to allow the borrower to have money now.

Inflation means that a dollar today is not worth a dollar tomorrow. Interest rates then make sure that the value of the dollar today is the same as the value of the dollar tomorrow.

When you take a loan from a bank, they charge you interest on that loan. Mortgages, car loans, and personal loans all attract different interest rates and this interest is how banks make a profit. At the same time, when you save money in the bank, you are loaning them money. They compensate you by earning you interest on your savings.

When you pay these loans, you can either pay them periodically or once-off.

Example A: Paid off at once

You borrow $10,000 from your colleague and she charges you 20% on that loan for a year. At the end of the year, you will pay her back $12,000.

The difference between how much you paid back and the amount you borrowed is the interest, which is calculated as $10,000 x 20% = $2,000. You then pay this amount off at once after one year.

Example B: Paid periodically

One example of periodically paid loans is mortgages. Mortgages are amortized. An amortized loan simply means that each periodic payment you pay back has both the capital (the amount borrowed) and interest amount embedded in it.

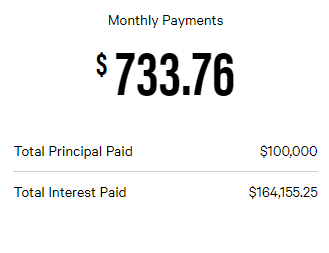

Let us assume you took out a mortgage loan of $100,000 for 30 years, at an agreed interest rate per year of 8%. Using a mortgage calculator, your monthly payments are:

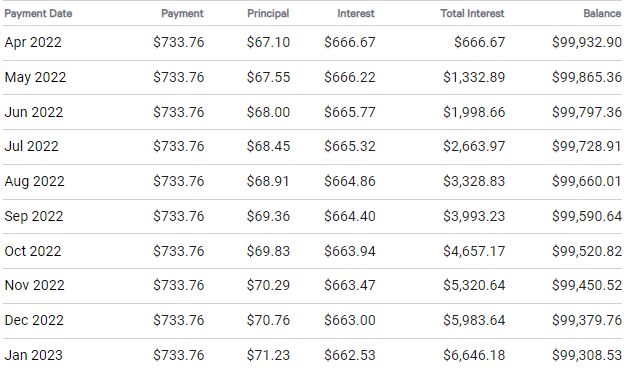

That $733.76 payment made each month has components of the interest and the principal in it.

In April 2022, $67.10 + $666.67 gives you $733.77. In Jan 2023, $71.23 + $662.53 gives you $733.76. All the way to the end:

In March 2052, you pay off the last loan installment and your loan balance ends.

The total amount you will pay throughout the life of the loan is $733.76 x 360 = $264,153.60. This amount includes the $100,000 principal amount and the difference is the interest. $264,153.60 – $100,000 = $164,153.60 is the interest.

A loan that is paid over many years is more likely to be amortized than a loan that is due in a month’s time. The longer the payback period, the higher the interest amount.

Interest can also be calculated on a simple basis or on a compounded basis.

How to calculate simple interest

Simple interest is similar to that in example A. To calculate simple interest, you use this equation:

A = P(1 + rt)

Where:

- A is the final amount

- P is the principal (or amount borrowed)

- r is the interest rate

- t is the time in years

So bringing back example A:

$10,000(1 + (0.2 x 1)) = $12,000.

If it was for two years, then it becomes:

$10,000(1 + (0.2 x 2)) = $14,000.

How to calculate compound interest

Compounding means earning “interest on interest”. Below is an example.

Example C

You borrow $10,000 for 2 years from your brother. He tells you that he will lend it to you at 20% interest, compounded annually, and after 2 years, you can pay the full and final amount.

In the first year, the total amount owed is:

$10,000 x 1.20 = $12,000. The interest is $12,000 – $10,000 = $2,000.

In the second year, the total amount owed is:

$12,000 x 1.20 = $14,400. The interest is $14,400 – $12,000 = $2,400.

A shorter way to calculate it is: $10,000 x 1.202 = $14,400

The interest in the first year is based on the principal amount borrowed. The interest in the second year is not based on the principal amount of $10,000; rather, it is based on the principal amount and the first year’s interest.

Comparing the final amounts of the simple interest and compounding interest, we can see the simple interest has an ending amount of $14,000 and the compounding interest has a final amount of $14,400.

Compounded investments are great when you are looking into your children’s education or your retirement.

If you are a lender (investor), you make more money from higher interest rates. From a consumer’s (borrower’s) perspective, you pay more when interest rates are high.

Inflation

Inflation is the rate of increase in prices over time. When inflation is ‘high’, the prices of items increase at an increasing rate. When inflation is ‘low’, the prices of items increase at a (s)lower rate.

Inflation erodes the purchasing power of money. Your grandparents could buy more with a $100 bill when they were your age than you can now.

Inflation also reduces your real returns earned when you save at a bank. If you keep your money in a savings account that gives you 4%, and inflation is 2%, then your real return is 2%. If the savings interest rate was 4% and inflation was 6%, then your real return is negative 2%; which means you are losing money by saving it.

This is part of why we invest — to beat inflation.

The inflation rate can be determined by a basket of goods. The basket of goods includes goods and services such as basic foods, oil prices, rentals and mortgages, clothes, and a range of services. Taken together, this makes up the Consumer Price Index (CPI).

There is the base CPI, and any other CPI after that is compared to the base CPI to determine the change in inflation. So if the base CPI is 6% in 2021 and 12% in 2022, we say that inflation has doubled (i.e., gone up by 100%).

Because these goods are bought by consumers, it illuminates the inflation borne by consumers. However, Inflation can also be viewed from the perspective of producers. This perspective gives us the Producer Price Index, or PPI. This index tracks production costs over time. As production costs rise, it passes down to consumers as an increase in goods and services.

By tracking the CPI and PPI, we can track the general level of inflation in the economy.

Causes of inflation

Demand-pull inflation

When the demand for goods or services increases more than producers can supply it, there is an increase in the price of these goods. Think of it as scarcity: a scarce item is more expensive than something which is available in abundance.

Let’s say there is demand for 100 gaming consoles a year. Game companies then produce those 100 consoles and sell them for $100 each. Let’s assume this production capacity is fixed.

Then, after a viral TikTok video, demand for gaming consoles shoots up and there are 200 pre-orders for gaming consoles per year. But production is fixed and it’ll take time to increase capacity.

So to manage demand based on limited supply, game companies raise the prices of their consoles to $200 each. This limits demand while they increase supply capacity.

That’s inflation in a nutshell; too much money chasing too few goods causes a rise in prices.

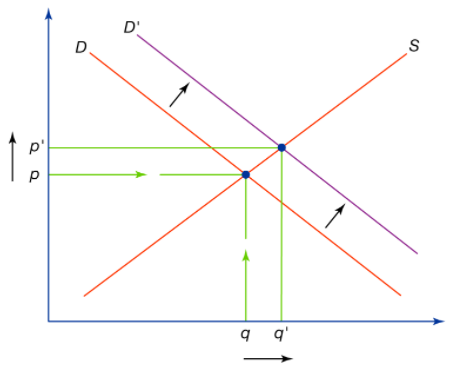

Demand-pull inflation occurs during times of economic booms. When the economy is booming, consumers have money to spend on many things. They demand more because they can afford more. Remember that from a demand-supply perspective, high demand translates to a higher increase in price (from p to p1), all things equal:

Cost-push inflation

When the unit cost of raw materials increases, producers increase prices to maintain a healthy profit margin. If a car manufacturer needs aluminum, and the unit cost of aluminum goes up, the manufacturer increases the price of the car to maintain their profit margin.

You can see cost-push inflation in situations such as the Russia—Ukraine war. During the war, certain commodities — wheat, oil, cobalt, and nickels — went up in price. Producers paid a higher price for these raw materials and passed on this increase to the consumer.

When wheat prices rise, it costs more to produce cereal, biscuits, pastry, and pasta, making them more expensive for the consumer.

The cost of these raw materials pushes the prices of goods up, causing inflation.

Wages are another variable that can cause cost-push inflation. If a corporation increases employee wages, this eats at their bottom line as it’s a cost to the company. Companies then raise the prices of their goods and services to account for those wage increases.

During times of low unemployment and an expanding economy, inflation happens because a healthy economy means that companies can afford to hire more people or increase wages. An increase in wages means an increase in prices to sustain those wage increases.

Central bank policies

Central banks also affect inflation levels. During times of low economic activity, central banks spur the economy by increasing government spending or reducing interest rates.

Remember that interest rates determine the cost of borrowing. If the cost of borrowing is low, businesses and people borrow more and spend more.

Low-interest rates also deter people from saving since they earn low interest on their savings, so they spend or invest instead. This increases economic activity — and if people are spending more money, demand for goods goes up, which increases prices of goods, all things equal.

Central banks pay attention to inflation, and if it gets too high, they move to correct it. This includes increasing interest rates so borrowing is more expensive and encourage people to save more so they can earn higher interests on their savings. By reducing the money supply in the economy, central banks can help curb inflation.

Interest rates, inflation, and investing

When investing, you need to take into account the type of investment (shares, bonds, property, etc), your risk appetite (cautious, balanced, growth), the state of the economy (recession or boom), inflation, and interest rates.

Interest rates and inflation play a critical role in how well your investments perform.

Interest rates and investing

When interest rates are low, companies can borrow more and do more. This grows the company and increases their profits, which translates to better share price performance. Low-interest rates also mean low-interest payments, which boosts their bottom line.

Another rationale is this: because interest rates are low, investors won’t want to save because they will get low returns. They would rather invest. This increased demand for stocks translates to higher stock prices.

Inflation and investing

Because inflation erodes the value of money, your investment return should be higher than the level of inflation. Taking advantage of sectors that benefit from an increase in inflation helps you. The commodity and energy sectors, for example, benefit from inflation as companies in these sectors can simply raise their prices and pass them on to consumers. An increase in fuel prices hurts consumers but benefits investors.

Investing in Treasury Inflation-Protected Securities (TIPS) also helps beat inflation. As inflation rises, coupons on TIPS rise as well.

Property is another area that protects you from inflation. If you own a house and inflation rises, you can increase the rental to account for inflation.

As an investor, you should take note of rising inflation because if it gets too high, the central bank will move to reduce it. Reducing inflation means increasing interest rates, which leads to reduced asset prices.

One sector that benefits from increased interest rates is financials – your banks, mortgage houses, insurers, etc. High interest is how they make their money, so investing in them helps you offset the decrease in asset prices of other sectors.

Take interest and inflate the performance of your investment

As a consumer or an investor, interest rates and inflation affect you. Understanding them allows you to make better financial decisions from taking a loan to investing in the stock market.

Enlisting the help of a financial advisor also allows you to make better decisions as they can advise you on which sectors to enter when interest rates and inflation are at different levels.