Have you ever sat and wondered how someone will support themselves in old age? Would it be from “Black tax”? Business income? A pension? Or will they work until the Grim Reaper calls?

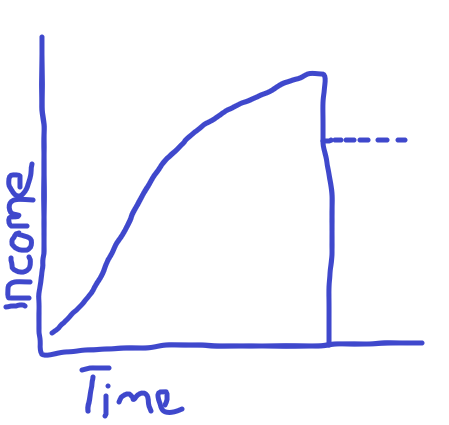

Everyone ages and will need money for retirement. Let’s assume Abel has a salaried job. At some point, the salary stops, and Abel will need to figure out how to support himself. Below is a poorly drawn diagram of what I mean:

As time passes, Abel’s income increases as he gets salary increases and promotions. However, when he reaches his retirement age, his salary stops coming in and he’d need to figure out a way to still have income well into his retirement.

In retirement, you need to have a good Net Replacement Ratio.

What is a ‘Net Replacement Ratio’?

The ratio of your income in retirement to your final salary is called the Net Replacement Ratio (NRR). It is calculated by dividing the annual income earned in retirement by the annual income earned in the final year of your salaried life.

For example, if in your last year of work, you earned 500,000, and in retirement, you earn 300,000 per annum, then you have replaced 60% of your pre-retirement income.

If your income was 100,000 post-retirement, your NRR would be 20%, and this likely means you didn’t manage your finances well in your working life. A good NRR is 70% to 85%.

Pension funds

Pension funds pool money together from members/employees and they invest the money in different countries and different asset classes.

Pension Fund trustees have a fiduciary duty to ensure the money is invested carefully and diligently. The third party that invests this money on behalf of the pension fund is the asset manager.

The asset manager’s duty is simple: make money, beat your benchmark, beat inflation.

Aside from asset managers, other stakeholders in the pension fund industry include:

- Actuaries assess and manage financial risks to ensure the stability and sustainability of pension funds,

- Auditors verify the accuracy and completeness of financial statements and transactions for pension funds to ensure compliance with regulations and financial integrity,

- Administrators oversee the day-to-day operations of pension funds, managing contributions, distributions, and member services to ensure smooth functioning and adherence to plan provisions,

- Asset consultants advise the fund on investment strategies.

Asset consulting

As an asset consultant, I help create sound investment strategies for the Fund. The strategies I create allow members’ money to grow over their working years. The strategy would take into account the risks and objectives of the Fund.

To do my job well, I work with some of the other third parties mentioned above, especially the Administrators and Asset Managers.

Below are the steps I take in creating your strategy:

Step 1: Needs Analysis

To make you money, I have to do a Needs Analysis. By understanding the members, who they are, how much their pension is worth, their age, etc, I can understand the objectives and risk appetite of the Fund.

By going through the membership data, I can ascertain whether the Fund is young or aging. There are two ways to determine this: through member age and fund credits.

A young fund will have more younger members than older members. An aging fund would be the opposite. “Young” and “Old” are all relative to the Fund’s set retirement age.

If the retirement age is 60, a 20-year-old is considered young. A 57-year-old is considered old. The pension fund determines what the retirement age is and what the switching age from young to old is.

Each member would have something called a fund credit. A fund credit is what the Fund would owe that member if they retired today.

When a member joins the company, they have few fund credits. As they stay longer in the company and contribute more, their fund credits grow, such that when they retire, they’ll have accumulated a good amount of fund credits. The size of a member’s fund credit depends on their salary, the time spent in the Fund, and the performance of the financial markets.

So for example, if a Fund has 1,000 members, and has a set retirement age of 60, with a switching rule of 5 years, then this means that members who are 54 and below are considered young and those 55 and above are considered to be old and close to retirement.

There are some cases where there are a few older members closer to retirement and they have a large fund credit due to them. In this situation, the Fund is considered aging, as it will need to pay out huge amounts to retirees soon.

Step 2: Market research

Next, I pore through financial market data to look at the different asset classes the Fund has agreed to invest in.

Some assets, like direct crypto, are too risky for the fund and are thus not allowed to be invested in. Other assets, like private equity, while risky, and have a long investment horizon, are allowable asset classes.

What a Fund can and cannot invest in is based on their risk appetite and the regulation within their jurisdiction.

I look for benchmarks that represent these asset classes. For example, I’d use the MSCI World as a proxy for Global Equities, SOFR for global cash, and the Domestic Company Index for local equities (if you lived in Botswana).

After I find the benchmarks for the allowable investment universe (what you are allowed to invest in), I then move to the asset allocation.

Step 3: Asset allocation

This step is the most critical.

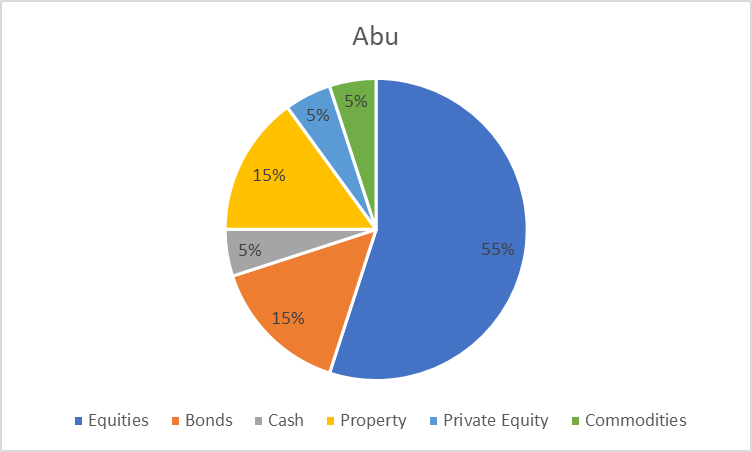

Allow me to explain this step using Abu and Zara. Abu is the pension fund with more young members with a higher fund credit. Zara is the pension fund with more older members with a higher fund credit.

Abu

Abu has a ways to go till retirement. He’s 30 and plans on retiring at 60. He can afford to take more risk.

Theoretically speaking, when looking at the different traditional asset classes, equities are considered the asset class with the most risk. Bonds come second, and cash is the safest.

Therefore, Abu will invest his money in the following proportion:

- 55% equities

- 15% bonds

- 5% cash

This is 75% invested in traditional asset classes. As we know of diversification, we’ll throw in some alternative asset classes: property, private equity, and commodity funds. The remaining 25% can be split as follows:

- 15% property

- 5% private equity

- 5% commodities

The way Abu’s portfolio allocation is set up is such that he’s taking more risk with the hopes of earning a high return over 30 years. He’s still diversified such that his portfolio reduces overall risk while enhancing returns. This differs from Zara.

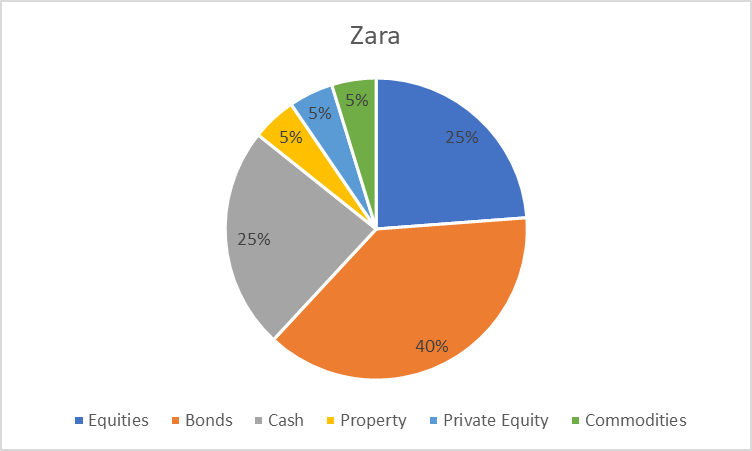

Zara

Zara is 57 years old and has 3 years to retire. Her main goal is to have a good net replacement ratio. Her investment objective would be safety but also brave enough to take enough risk to beat inflation.

Her portfolio would look thus:

- 25% equities

- 40% bonds

- 25% cash

- 5% commodities

- 5% property

Her portfolio has a higher allocation to traditionally “safer” assets. The other riskier assets are to ensure that she’s not too conservative that she misses out on good returns.

Abu and Zara are an illustration of how different Funds with different needs would be catered for.

Step 4: Asset managers

To ensure the above strategic allocation is carried out, I engage and liaise with asset management firms who would invest the Fund money according to the agreed-upon strategy.

The asset allocations above are called the “Strategic Asset Allocation” (SAA) and the asset managers would try their best to be in line with the percentages of the SAA. This is their benchmark. Their goal is to beat it and to also earn returns above inflation.

They have the discretion, however, to deviate away from their benchmarks. They shouldn’t deviate from it too much or for too long, however.

For example, an asset manager might deviate from the SAA if they feel a recession is coming. If a recession hits, holding too much equities might be bad for the Fund. So they will sell and hold more cash or bonds.

If the manager expects inflation to skyrocket, energy prices might go up, and if central banks increase interest rates, bond prices will go down. So the manager might reduce their bond holdings and put more in commodity funds temporarily.

While the asset consultant creates the overarching strategies, the asset managers are the ones who drill further into the actual stocks and bonds to buy and sell.

The asset managers implement the investment strategy; where to invest, what to invest in, and in what proportion.

Step 5: Monitoring and evaluation

Investing is a long game. When members invest, they have to wait several years and let compounding do its thing. After implementation, the strategy has to be monitored and reviewed regularly (usually 3 years).

For example, before technology became a thing in our stock markets, financial, energy, and manufacturing companies were among the few profitable sectors. Now things have evolved and so your strategy must evolve too.

Time and regular reviews are key in ensuring the strategies put in place are bearing fruit.

Get started

Reach out to an asset consultant to help you create investment strategies for your pension fund. Remember that the asset allocation is what you need to get right.

Seeking the help of a professional can assist with that, looking at your risk appetite, investment horizon, and many other factors.

The ultimate goal? Improving the NRR of the members you promised to take care of.