What is a ‘Motshelo’?

In the West, they call it ‘pooled funds’; in southern Africa, they call it a ‘Stokvel’ (South Africa) or Motshelo (Botswana).

This financial scheme takes advantage of the power of numbers by having people pool funds for different economic purposes. These purposes can be for saving, investing, burials, lending, and even buying groceries.

This article will describe how a Motshelo, created for the purpose of loaning out money, works.

A loan-based motshelo system

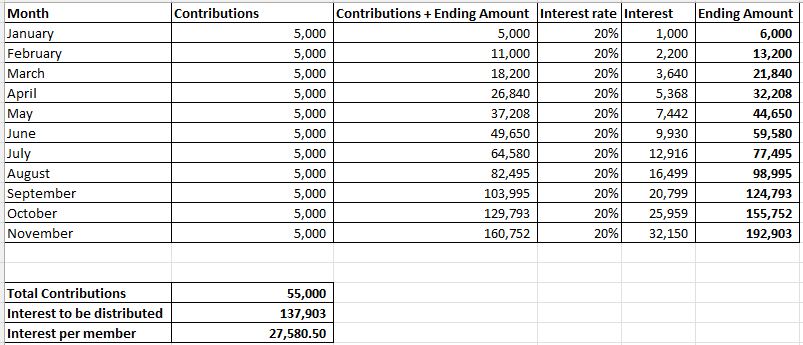

Imagine a Motshelo with 5 members, each contributing P1,000 at the end of each month. This brings the total monthly contribution to P5,000. The members agree to lend this money to people outside the Motshelo (Non-Members) at 20% per month, compounded.

In a scenario where the full P5,000 is lent out to several trustworthy non-members for a month, the total amount brought back at the end of the month is P6,000, which comprises P5,000 principal and P1,000 interest. Let us call this Month 1.

In Month 2, the Motshelo now has P6,000 available to loan out. But also remember that contributions are monthly. So the P6,000 comes back, and another P5,000 is contributed. The amount sitting in the Motshelo is now P11,000.

Let us assume that the members manage to lend out the entire P11,000.

At an interest rate of 20%, if every non-member pays back what they owe, the amount that comes back is P13,200, which comprises P11,000 principal and P2,200 interest.

With P13,200 in there, plus another P5,000 injection, the Motshelo has more money now to lend out.

Here is a table showing how everything would be if everything went right. I put that in bold because there is a saying that goes “Madi a jelwe ke dipeba”, which loosely translates to, “Rats ate the money”. This happens when there is fraud within the Motshelo, but more on that later.

(Note: The contributions are made at the end of each month. The last contribution happens at the end of November and the money is distributed in December, just before the holidays).

Looking at this table, if all monies were loaned out each month at 20%, at the end of the year, the money available to be distributed amongst the members would be P192,903. We can say that P192,903 was made from a contribution of P55,000. That’s approximately a 232% return.

Each member walks away with their contribution of P11,000 (P1000 for 11 months) plus their interest share of P27,580.50, giving a total of P38,580.50

Imagine that: you put in P11,000, and you walk away with close to P40,000. That’s the power of numbers!

If you had just saved the P11,000 in a bank, your returns would be significantly lower.

Things that might go wrong with your Motshelo

A number of things can go wrong that would deter the Motshelo from reaching its goal of P192,903.

- Defaults – the borrowers may default on their payments.

- Opportunities Lost – In some months, not all the money will be loaned out, meaning not as much interest will be earned.

- Fraud (The Rats!)

- If you have dishonest members, they can decide to lend the money out to people and when those people pay it back, the member doesn’t send it back to the Motshelo account. They pocket it for themselves.

- The accountant handling the funds may also decide to do unscrupulous activities and eat the money.

- Non-existing borrowers: Some members will lie and say that they have someone who needs to borrow money when in fact, there is no one. They just want the money for themselves and won’t pay it back.

4 ways to mitigate Motshelo risks

How do you mitigate the risk that something might go wrong?

- Contracts – Signing contracts reduce the chance of fraud and defaults as people may fear getting in trouble with the law.

- Background Check – Not everyone has the capacity to pay what they owe. Some people have debt issues. Asking for a payslip or bank statement allows you to see their spending habits. Bad spending habit is bad for business.

- A Cap – Having a low cap on how much money you can loan out manages the losses if a borrower defaults. If you have a cap of P2,000 that you can loan out to each individual, it means that if they default, you lose P2,000. Now imagine if there was no cap and you gave them P10,000, and they default. “Nka Screama Gore” (loosely means “😱”).

- Bank, Not Cash – Using bank accounts allows a paper trail to be formed. It also allows for easier auditing and proof in case any fraudulent activities take place.

How to spend Motshelo funds

I would be remiss if I did not give advice on how to wisely spend the P38,580.50 that you would be receiving around the holiday season.

- Save and Invest – set aside a chunk of this and put it in an investment account for your long-term investment. For your short-term emergency needs, invest in a money-market account.

- Pay Debt – Use it to clear some small debts or put it towards reducing your larger debts.

- Budgeting – Rent, utilities, school fees for your kids, and other expenditures need to be paid. If you want to have a stress-free January where you don’t want to worry about electricity, water, rent, wifi, school fees, etc coming from your salary, use your Motshelo payout. That way, your December salary can be stretched out in January because as we all know, January has 100 days.

- Spoil Yourself – money is meant to be spent. It’s the holiday season and if you’ve been saving up for a trip or that new gadget or that new outfit, spoil yourself.

- Do Not – if you and your members agree, don’t touch it. Instead, roll the funds into the next year and make even more money. This is usually done for large capital-based investments like property investments.

Motshelo: Providing power in numbers

Motshelos are meant to help individuals be more disciplined, save, invest, and prepare for any life emergencies. The more members, the greater the chance of higher returns. In as much as it has risks since you are dealing with human beings, if all goes well, the returns are well worth it.

Spending the payout wisely is also paramount in your financial planning journey. Reach out to a financial advisor to help you manage your payout!